Stay up to date with notifications from The?Independent

Notifications can be managed in browser preferences.

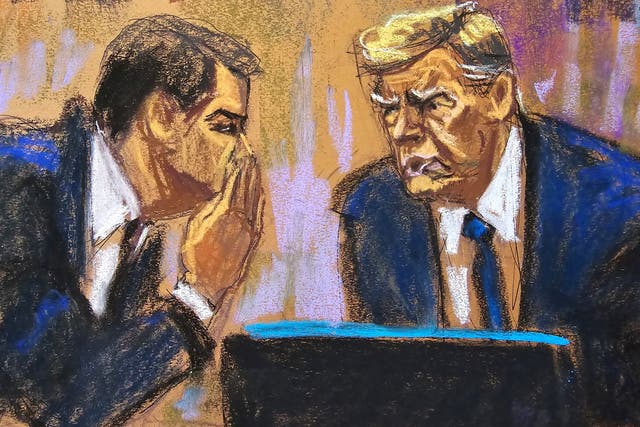

Trump on trial

trump on trial

Two seated jurors struck from Trump hush money trial

Top stories

politics

Mike Johnson gambles everything while a far-right rebellion grows

The speaker’s complicated plan to split aid for Ukraine and Israel into four separate bills might not be enough to quell what’s happening in Congress, John Bowden reports

climate crisis

Does anyone care about climate this election? These voters say yes

The majority of Americans have experienced extreme weather events in the last five years — but the climate crisis still lags behind inflation, healthcare, immigration and jobs when it comes to voter priorities. Louise Boyle reports

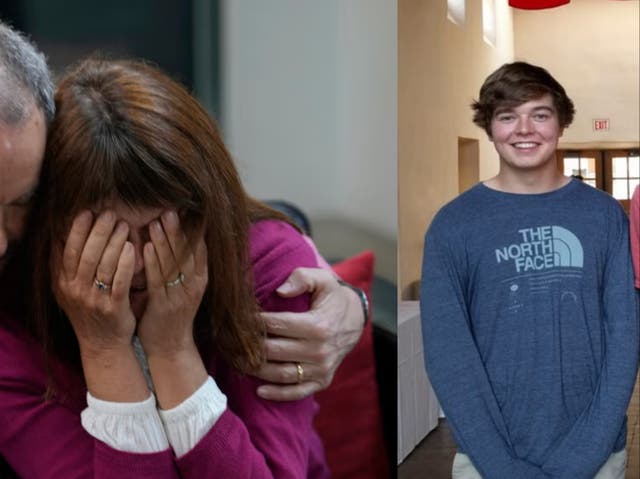

Livechad daybell

Chad Daybell trial: Cult dad’s search history revealed to jurors

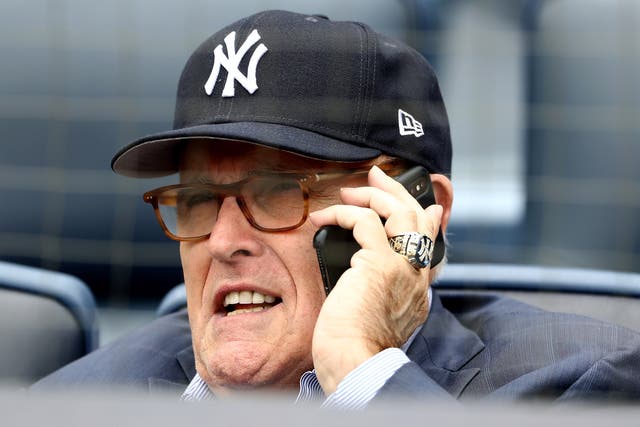

rudy giuliani

Giuliani’s bankruptcy could cost him his apartment, his jewellery and, perhaps worse, his Joe DiMaggio shirt

From multimillion-dollar properties to luxury watches (and a replica signed Joe DiMaggio shirt), the former New York mayor and Trump attorney may have to part with some cherished items to pay his creditors, writes Kelly Rissman

featureTech

Video game creators scramble to unionize as AI threat looms

As the gaming industry reels from a tidal wave of layoffs, companies’ rush into automation has developers watching their backs – and could soon trigger a major strike. Io Dodds reports

news

Six arrested over Canada’s ‘largest’ ever gold heist worth $20m

‘This story is a sensational one, and one which probably, we jokingly say, belongs in a Netflix series”, Chief of the Peel Regional Police Nishan Duraiappah said

TECH

Lifestyle

Culture

Travel

Tech

Sport